When loan payments pause, business potential soars

Get funded in 24h. Pause repayments when your business needs it the most. Maximise business opportunities when it matters.

The result? Space to grow your business with the funds you need. Zero interest accrues during the payment pause.

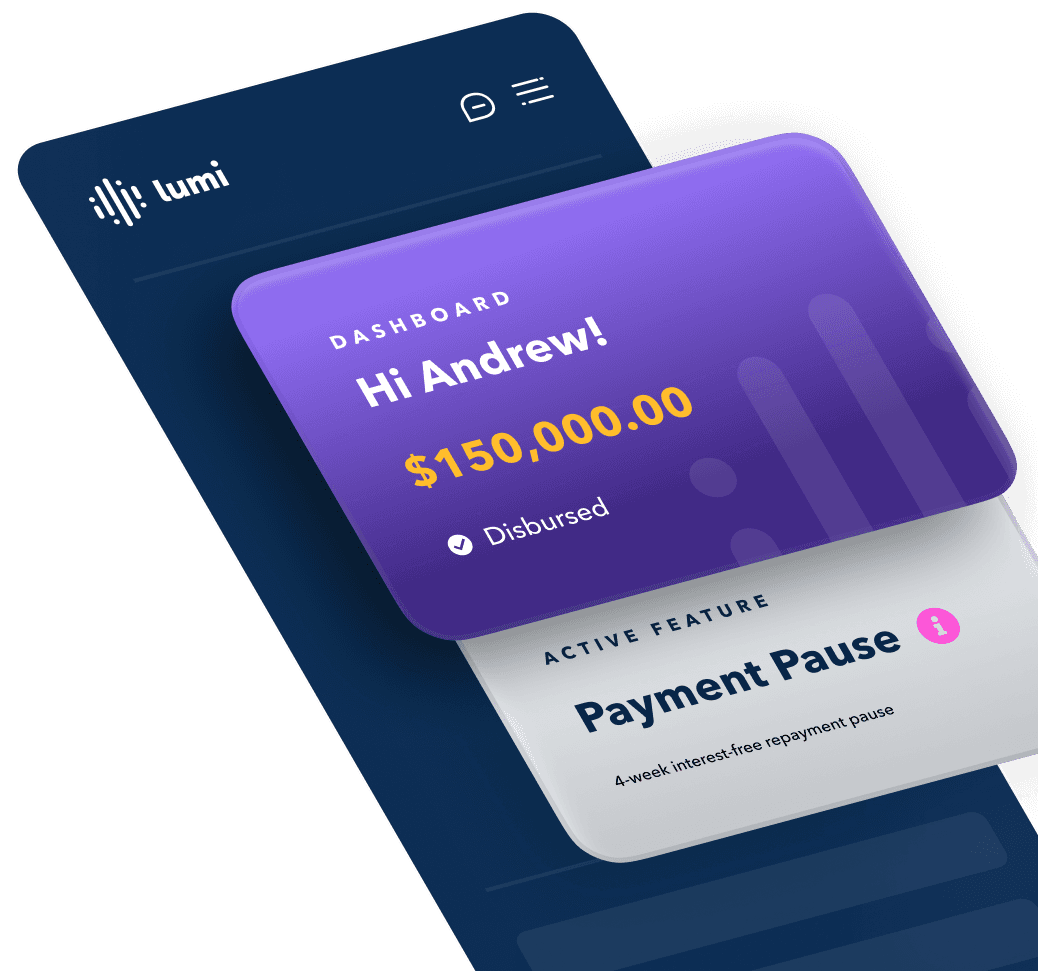

4-week interest-free payment pause when your business needs it most

Get ahead by prioritising your business over repayments

Free up money to put back into what matters

1. Check your eligibility

See if you qualify for a Lumi Business Loan with Payment Pause in under 2 minutes.

3. Pause repayments when you need it most

For up to 4 weeks to boost cash flow and maximise business opportunities.

Frequently Asked Questions

Terms & Conditions

Lumi Payment Pause applies to new term loans only (not lines of credit). Approval of a Payment Pause is at Lumi's discretion and requires meeting all contractual obligations.

All loan products are subject to eligibility and approval.

For Businesses

Fast access to finance that fits your business.

For Brokers

Fast funding with fair rates for your clients. Competitive commission for you.

For Platforms

Fast funding for your clients. New revenue streams for you.